AI & Real Estate: Beyond Generative

The direction is obvious. The speed is what breaks you.

The latest module for #GenerativeAIforRealEstatePeople runs to 9,000 words. This is the core argument, compressed. Course participants get the full version with the scenario frameworks, asset-class analysis, operational horizons, and the uncomfortable questions at the end.

The thesis in one sentence

The direction of AI in real estate is largely knowable and mostly uncontroversial. The variable that determines whether your assets appreciate or depreciate is speed of arrival - and the industry has no framework for assessing it.

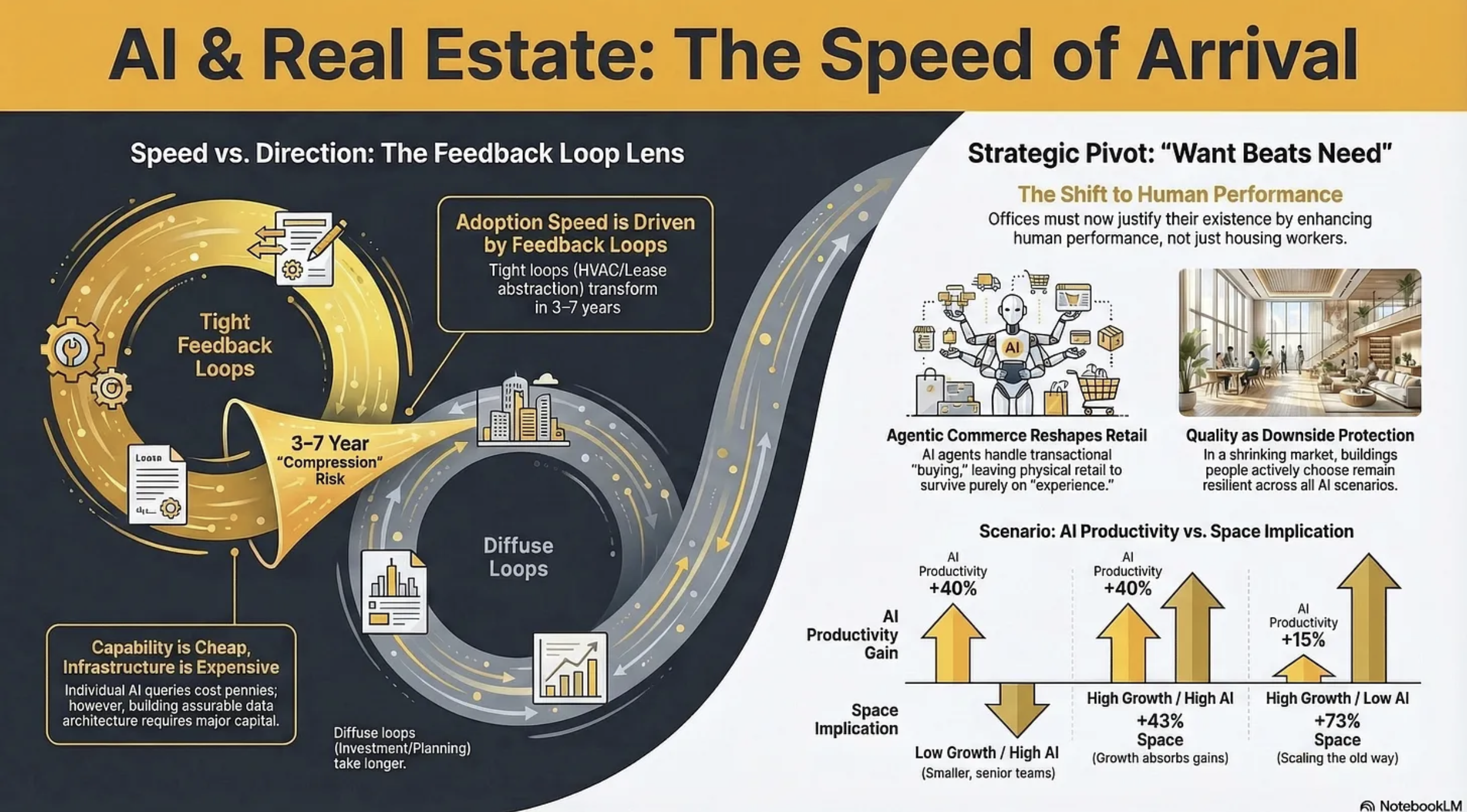

Why speed, not direction

In 2023, esteemed AI researcher Andrej Karpathy published a diagram showing an LLM as the kernel of a new operating system. Most people read it as a five-year forecast. It arrived in roughly eighteen months.

If the market has 10–15 years to adjust to AI-driven change, outcomes are manageable: portfolios rotate, buildings retrofit, organisations retrain, capital markets reprice gradually.

Compress the same changes into 3–7 years and you get stranded assets, workforce dislocation, and the kind of repricing that destroys value for anyone who moved too slowly.

The course module introduces a predictive lens for this: feedback loops. Domains with tight feedback loops - where you can quickly and objectively measure whether the AI’s output is correct - transform fast. HVAC optimisation, lease abstraction, code generation: these are already being reshaped. Domains with diffuse feedback loops - investment judgement, tenant relationship management, urban planning - change more slowly and less predictably.

For CRE professionals, this creates a split reality. The operational and transactional layers sit in the tight-feedback category. The strategic and relational layers sit in the diffuse category. But the operational transformation inevitably changes the context in which strategic decisions are made. You cannot hold the two apart for long.

What has changed since the first version of this module?

Three of the four original barriers to AI adoption have shifted:

The cost barrier has flipped. Individual AI inference is now negligible. But deploying AI at enterprise scale - the data architecture, integration middleware, cybersecurity, governance - is a serious capital commitment. The firms that understood this early allocated 20% of their AI budgets to technology and 80% to change management. Most did the opposite. Some are still debating whether to start.

Data quality matters differently. Frontier models handle messy, unstructured data remarkably well. The constraint has shifted from “our data isn’t clean enough for AI“ to “our data isn’t structured enough for assurable AI.“ AI can work with your data. The question is whether the outputs are auditable enough for board-level decisions and transaction sign-offs.

Agentic AI changes the integration calculus. The industry’s systemic fragmentation remains real. But AI agents that autonomously navigate between software platforms, APIs, and data sources mean the integration problem is becoming solvable without requiring the entire ecosystem to adopt common standards. This changes the cost-benefit calculation for early movers - which is exactly the dynamic that creates competitive advantage.

What has not changed: deep institutional inertia, fragmented ownership, long asset cycles, misaligned incentives. The destination is locked in; the uncertainty is pace.

Two forces, one asset

The module’s central analytical framework distinguishes two ways AI affects commercial real estate - and then immediately insists you cannot treat them separately.

AI acting ON real estate: new demand patterns, new asset classes, structural shifts in what gets built and where. A capital allocation question. Speed is outside your control.

AI used BY real estate: how existing assets are operated, transacted, valued, and experienced. An operational alpha question. Speed is a competitive variable.

The critical insight is that these are not separate categories to sort assets into. They are competing pressures acting on the same building simultaneously. A prime office is shaped by AI acting on it (changing occupier headcount, raising specification expectations) and by AI used within it (smart building systems, personalised tenant experience, automated FM). The investment outcome depends on whether the owner is deploying AI fast enough to offset the structural pressures AI is creating.

Need declines. Want is what remains.

The deepest argument in the module - the one that sits beneath every section - is a shift in the nature of real estate demand itself.

If AI absorbs the routine knowledge work that currently fills offices, the purpose of the office shifts toward collaboration, mentoring, culture-building, creative work. The same logic applies to retail (experiential over transactional), healthcare (patient-facing over administrative), and any asset class where the human element is the value proposition.

The fundamental question shifts from need to want. And that changes everything about underwriting.

Need-driven demand is predictable, stable, and relatively insensitive to quality. Choice-driven demand is volatile, quality-sensitive, and ruthlessly comparative. An office is no longer competing only against other offices. It is competing against the increasingly viable alternative of not having a central office at all. When the benchmark shifts from “the next best office” to “not having an office,” the bar for what constitutes a compelling offer rises dramatically.

This is uncomfortable for owners of average stock. But it contains a genuine opportunity: you can still win big in a shrinking market if you are building something people actively desire. The polarisation between best-in-class and everything else widens. Quality becomes not just a return enhancer but downside protection protection.

The asset-class implications (in brief)

The full module works through offices, data centres, logistics, healthcare, retail, and four residential sub-sectors. A few highlights:

Offices get a four-scenario framework crossing output growth with AI productivity. The same AI capability can mean 22% less space or 43% more, depending on whether the occupier is growing. No macro model tells you which scenario you’re in. Only your occupier’s specific context does.

Retail confronts agentic commerce - not just e-commerce, but AI agents that research, compare, and purchase on your behalf. This is more destructive to average retail than e-commerce was, because it removes the last functional justification for visiting a mediocre destination. But it simultaneously purifies the demand signal: everyone who walks through the door is there because they want to be.

Logistics gets an agentic commerce multiplier: even if consumer spending stays flat, the volume of goods flowing through fulfilment channels likely increases because agents eliminate the friction that currently constrains transaction volume. The module is honest about the returns question - net effect on return volumes is genuinely uncertain - but the specification requirements for logistics facilities are rising regardless.

Later living has arguably the most compelling operational AI case of any residential segment, because the applications are care-critical, not merely commercial. Health monitoring, predictive intervention, fall detection, loneliness mitigation. AI does not just improve efficiency; it changes the care proposition.

The geography argument

AI may be doing something more subtle than the pandemic’s failed decentralisation prediction. The pandemic proved remote work was technically possible. AI is making it technically excellent. The justification for being in a specific place shifts from “I need to be here to do my job“ to “I choose to be here because the environment is worth the commute.“

The e-commerce parallel is instructive. Online retail didn’t uniformly undermine physical retail. It reshaped its geography - devastating locations that competed on convenience while boosting locations that competed on experience. AI may do the same to office geography: devastating locations that competed on proximity to work while boosting locations that compete on quality of place.

The operational horizon

The module includes a compressed reference map of twelve capabilities across three time horizons (now–2yr, 2–5yr, 5–10yr), classified by feedback-loop type. The tight-feedback, near-term capabilities - HVAC optimisation with sub-one-year payback, AI lease extraction, occupancy intelligence, agentic FM triage - are proven, measurable, and deployable now.

And this produces the module’s sharpest irony: the industry spends most of its analytical energy debating the things it cannot control (will AI reduce office demand by 10% or 20%?) and has not yet deployed the things

it can. The storm is uncertain. The ship-building is not.

What replaces confident forward projection?

The module argues that the pretence of confident 3–5 year NOI projection is becoming actively misleading when the variance of plausible outcomes has widened this dramatically. What replaces it:

Scenario discipline over point forecasts. Not new, but the variables that matter have changed. AI productivity and occupier growth posture are not factors that appeared in traditional CRE stress-testing.

Optionality over commitment. When the range of outcomes is wide, assets and structures that preserve flexibility are worth a premium. The traditional preference for long leases and stable income is a bet on low variance. If AI delivers high variance, that bet loses.

Occupier intelligence over market-level data. The edge moves to granular understanding of individual tenants - their growth trajectory, their AI posture, their industry dynamics.

Quality as insurance. Buildings people choose to occupy are resilient across more scenarios than buildings people are forced to occupy.

Supply constraints and market inertia are not a strategy. They are a sedative.