THE BLOG

Brexit will turbo charge the technology industry and radically change real estate

July 2016

The U.K has had its referendum and voted for Brexit. We are assured that ‘Brexit means Brexit’, so unless something unexpected happens (which given the last two weeks would by no means be unexpected) we will leave the EU, ‘take back control’ (sic) and reduce immigration to the tens of thousands, as was promised in the Conservative Government’s Manifesto.

And at that point the U.K economy will change, quite dramatically.

Several industries have high concentrations of overseas workers: processing plants at 43%, cleaning and housekeeping at 34 % and hospitality and retail with 30%. And they are not alone. 16.7% of ALL employees are foreign born (2014 figures).

Now we can argue about how quickly and to what degree these numbers diminish, but it is safe to say that many will not be here in 3-5 yrs, and certainly not that many new immigrants will be arriving. The people have spoken, and this will be the result.

So what, in Economics 101, happens when labour becomes scarce or rises in price? Yes of course, it gets replaced by Capital. At a certain point the cost of automating a process crosses below the cost of employing someone. And what is happening in the world of automation, robotics, machine learning and artificial intelligence? Yes, it is very rapidly becoming very much cheaper to do very much more each year. Put the two together and what is the result? The automation of jobs currently performed by inexpensive migrant labour.

UK workers will not benefit from all their jobs no longer being taken by migrants. The jobs will simply disappear in a tsunami of automation.

Fully automated McDonalds already exist. Amazon has spent billions on warehouse robots. Machines can deal with just about every agricultural task. Room service robots are already out there and self driving cars are improving by the day (Tesla crash notwithstanding).

Data is moving to the Cloud, high speed connectivity is becoming ubiquitous, and just about everyone has a 1990 Cray Supercomputer in their pocket. Add to that billions of ultra low cost sensors being deployed into just about everything, and we have the ingredients for replacing vast amounts of Labour with Capital.

And with Brexit we have the incentive to push the button on doing just that. When motive meets opportunity and capability, then big changes can happen very quickly.

So the tech industry is going to find itself swamped with business to automate tasks out of existence. Whatever can be automated will be automated. And according to McKinsey 45 % of ALL work tasks could be automated with technology available today.

In parallel to all this new technology being developed will be the re-thinking and re-purposing of large amounts of real estate. Fully automated warehouses take a different form. Fast food outlets without the ubiquitous overseas staff will be redesigned (in how they look and how they work), and retail will morph into something very different to today. Customers will continue to demand a great experience when they shop, but how that is delivered will have to be re-designed. And it will be.

And you know what, the end result is likely to be better than now: clever use of smart technology coupled with far fewer (but better paid) staff will force retailers to up their game. With cheap labour available on a pay for what you use basis (zero hours contracts etc) the whole game is to be cheap. With expensive labour, the race to improve productivity is intense. And if you use technology wisely you can of course raise the productivity of any individual dramatically.

Furthermore all this new technology will hasten the move to offices being places where humans go to do what humans do best, rather than as knowledge processing ‘white colour factories’. See my earlier article ‘The Office is Dead’, Long live the Imaginarium’ for more on this. http://antonyslumbers.com/2023-the-future-of-real-estate/

So, big changes ahead. Turbo charged by Brexit. Was this what most ‘Brexiters’ voted for? Probably not. But as they say ‘actions have consequences’.

Antony

Real Estate: Equally Cursed and Blessed

June 2016

The Real Estate Industry is equally cursed and blessed. That was my overriding feeling following a day at the FUTURE: PropTech conference a couple of weeks ago. Blessed because nothing much is changing in terms of how the industry works, but cursed because something much bigger is coming down the tracks.

First, the upside. Residential is not my area but for all the talk of ‘disruption’ the industry is largely the same as it was a decade ago. The vast majority of people use a traditional estate agent and list their properties on the portals. The online (or Call Centre as I’ve heard them disparagingly called) agents have spent a lot of money but not got very far. Truth be told most people are more bothered about getting the very best price for their homes than saving a small % in fees, and that fear of losing out (a primal human instinct) is hard to counter. Yes there are new marketing tools (VR will be big, though perhaps niche until smartphones become our VR devices) and it is imperative for EVERY agent to offer first rate technology at every touchpoint of the consumers journey, but is the residential market being disrupted? An emphatic NO.

The Commercial industry, my area, is being changed even less. Public data sets are only slowly becoming available, the agents guard their own data, and even now there is no good search system available for ‘Joe public’. On top of that it is estimated that a third of the worlds real estate assets are still managed via spreadsheets. And judging from many of the comments at FUTURE: PropTech, surveying firms are adamant that that is how they wish things to stay. The industry mindset is still very protectionist, and any notions of free and open markets growing faster than closed ones is dismissed, often angrily. In this world, the primacy of the Lease is everything and the thinking goes that if data surrounding Leases is closely guarded then the industry has little to fear from ‘Disruption’.

So an industry truly blessed; the mechanics of the market are stacked in the favour of incumbents. Let the good times continue.

Ah, but life is not fair; you knew there would be a catch didn’t you? And there is. A big one. You see, most successfull companies do not fade or die because someone comes along and does what they do dramatically better than them. Once powerful and on a sustaining path, incumbents are very hard to shift. “Weebles wobble, but they don’t fall down”, as has been said. No, the real threat is always from something coming along that changes the value of exactly the thing these companies do do. The danger is that the market changes and one is stuck producing a product, or service, that whilst brilliant, and efficient, is simply no longer desirable anymore. The PC killed the Mainframe and Mini Computer (DEC, Wang), the smartphone the mobile phone (Nokia) and the compact camera (Jessops), Uber the taxi business.

And this is what is going to happen to the commercial real estate business. It is not that Lease data, (and all that sits atop it) will suddenly become open source, and publicly available, and in doing so open up the industry to a wave of competition that will destroy margins, or empower customers to route around the advisory services they are currently lavishly charged for today. No, the point is that the Lease itself will go the way of the Dodo, becoming something that is simply no longer fit for purpose. Now, not entirely of course as a decent chunk of the market (top end, large corporates) will still require large amounts of space on secure long term terms. But the business landscape is becoming ever more barbell shaped – large numbers of big and small companies, with a diminishing number of mid sized firms. 80% of city of London based businesses have fewer than 10 employees. Just 205 employ 250 or more. As this trend develops do you really see long leases remaining relevant? Serviced office space has quadrupled in the last twenty years; factor in the growth of Co-working (which plays to multiple primal human instincts) and it is not hard to envisage a majority of space being occupied ‘as a service’. It is already commonplace to use ‘Software as a Service’, transportation (Uber) ‘as a service’ or accommodation (AirBnB) ‘as a service’. Why on earth not workspace?

All of which means many traditionally minded commercial real estate players are protecting a market that is (whisper it quietly) dying. The seeming normality of the industry today is very much flattering to deceive. The curse that is yet to be felt is merely sotto voce.

There is though another blessing out there. and that is that the entire technology landscape is moving from hardware and software to services, and the death of the Lease fits in with this trend. The smartphone may only be nine years old but essentially it has been perfected; witness the moans that the iPhone 7 is likely to look near identical to the iPhone 6. The format conundrum has been solved (Blackberry tried a square phone – it sold about 3 of those) and on device processing speeds are at near physical limits. So where does the industry go from here? The answer is services: natural language voice control is the next big thing in interface design. Instead of typing onto a keyboard we will increasingly just talk out loud. Google Amazon Echo for a foretaste of this world. This device is US only for now but, along with the newly announced Google Home, is a pointer to what having a PA (personal assistant) means in the late twenty teens. We thought the age of robots and artificial intelligence would look like something out of The Terminator, instead it looks like something from Heals.

What has this to do with commercial real estate? Everything. We all have a supercomputer in our pocket and the worlds knowledge available on demand. And this is changing all our aspirations; increasingly we crave experiences, not ownership. And what we’ll spend our money on is wrapped up in one word, services. Everything ‘as a service’, collaboratively so. Because what we can afford to do together is more than we can do apart. So I may only have 10 work colleagues but we all want to work in great spaces. We don’t need them all the time though, as our work and interactions with colleagues, clients and suppliers can happen from anywhere. And because we don’t need them all the time, we are prepared to pay much more for a great experience during the lesser number of hours we do. Coffee used to be cheap and from a pot; now it is expensive and presented to us by a Barista. We don’t care if the price is triple what it was; the experience is what we value.

Technology changes behaviour, not the other way around, and it is becoming invisible. Great spaces have a rich, but hidden, digital layer that enlivens them and makes them much more appealing places to be. The technology is allowing us to become more human, with far less restraints than historically. And the big restraint that we no longer want is the Lease. So it will die.

Once the industry figures out a new financing and investment model for this world it will explode. Freed by technology the real estate industry will enter a golden age. Different but much better.

Digital Strategy No 5: The dirty secret about innovation

April 2016

There is a dirty little secret about innovation; it doesn’t require much inspiration. Having a ‘Eureka’ moment like Archimedes is, by and large, not necessary. So anyone who has ever thought they could not innovate because they haven’t had any special moments of inspiration need not despair. Innovation is largely the result of systematic process, and everyone can learn that.

If you follow the startup world you will know that the best new companies work with a set of tools that to the wider business community are not that well known. These are:

1. The Business Model Canvas

2. The Value Proposition Canvas

3. Lean Startup Methodology + Agile development

4. Design Thinking/Sprints

5. Systems Thinking

Lean Startup author Eric Ries famously wrote “A startup is a human institution designed to create a new product or service under conditions of extreme uncertainty.” and the tools above are aimed at removing as much of that uncertainty as possible. Their applicability though is across the board; established businesses may have different dynamics to start ups, but the ongoing prosperity and survival of any business involves creating or improving products or services. These tools really help.

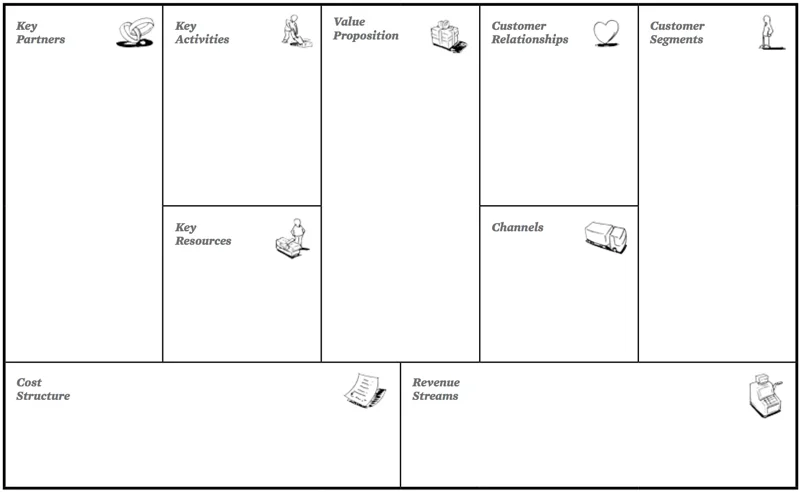

1. The Business Model Canvas

Created by Alexander Osterwalder, this is a visual chart that splits your business model into 9 segments, and in doing so allows you to really focus in on the fundamental purpose and viability of your business. The nine segments are:

1. Value Propositions

2. Customer Segments

3. Costs

4. Revenues

5. Channels to market

6. Customer Relationships

7. Key Partners

8. Key Activities

9. Key Resources

Points 1 & 2 are expanded on below but the beauty of this process is that it forces you to distil your business down to fundamentals, and encapsulate it on one slide or sheet of paper. Unlike a 50 page business plan, where discursion is the norm, the Business Model Canvas is powerfully transparent. If it does not look good here, then you better start planning for change. It can be a chastening exercise to run your own business through this; maybe it isn’t as strong or sustainable as one thought (or more precisely probably never actually thought about – in depth).

2. The Value Proposition Canvas

Extrapolating points 1 & 2 of the Business Model Canvas, here you address what your value proposition is, and whether or not it addresses customers who have real goals, real pain points and real beneficial requirements. Again the point is to surface strengths and weaknesses in your product or service. So many products address imaginary needs, miss areas where they could really add value, or go after customers that in practice do not exist, or are unlikely to ever be profitable.

3. Lean Startup Methodology

Once you have negotiated the two hurdles above you need to get your product or service into a state where it can be put in front of a real customer. As Steve Blank has said “No business plan survives first contact with a customer”. The Lean Startup Methodology is all about not wasting your time on things that do not matter. And it does that by taking you through a process where you get your product or service in front of a customer, learn from the encounter, and iterate until you have something with strong and sustainable ‘Product/Market Fit’. Build/Measure/Learn – and repeat. Honestly measure what matters and test all your assumptions. Business does not have to be boring, but it does have to be rigorous; the goal is to work on what works, and to not waste your time.

4. Design Thinking / Sprints

Steve Jobs said “Design is not just what it looks like and feels like. Design is how it works.” Few people seem to understand this. So often in business one encounters people who think of design as logo/colours/font and that is if they even think of font. Which is why the world is full of badly designed products, services and environments. Design thinking is a systematic approach that follows five steps: Empathise, Define, Ideate, Prototype and Test. You start off by working out who is your customer and what matters to them. From there you define their needs and ideate as many possible solutions as you can come up with. Then you filter these down to your best guess as to the number one option, prototype it and put it in front of a customer. You will then find out what worked, or didn’t, what hypotheses you had that were valid and which were plain wrong. Then, in the spirit of Build/Measure/Learn you repeat the exercise until you get it right. Though there is no absolute right. This whole process should be standard operating procedure in your company, something you do on an ongoing basis. After all the world moves on, doesn’t it?

Google use a variation of design thinking that they call design sprints. Where there is a particular issue, or service, or product to be dealt with they gather together everyone who might have an impact on the matter, and through a ‘Sprint’ lasting five days they collaboratively work their way through an intense ‘design’ process that culminates with controlled interviews with customers. This process allows for decision making time to be compressed dramatically. What might take months being discussed and moved down a decision tree is thrashed out in just a week through the not so simple expedient of forcing everyone who counts to focus on just one thing for five days. In ‘Get Things Done’ terms it wins top marks!

5. Systems Thinking

Lastly, Systems Thinking “is the process of understanding how those things which may be regarded as systems influence one another within a complete entity, or larger system.” So for example, if you are involved in the world of Smart Cities you need to look at how changes to transport networks affect pollution levels and energy usage. If you are developing software you might need to consider how taking one approach in a ‘standalone’ module would be much more impactful if it were linked to another hitherto ‘standalone’ module. It is the ‘no man is an island’ principle; everything is connected, although often in subtle ways that are missed unless one consciously looks out for such connections. Systems thinking is about zooming out and seeing the big picture, but as with everything discussed here, the process is iterative. You zoom in, then out, in then out. In mature industries you can pursue six sigma and aim to design out any inefficiencies or superfluous costs. In the world described above the assumption is that life is fluid, ever changing and ever demanding that we change and flex with it.

So there you have five very powerful tools to build, sustain or grow your business. As every business is becoming a digital business they should be an active part of your digital strategy.

Digital Strategy No 4: Data, analytics and the big but

April 2016

It was the great St. Thomas More who first referred, in 1532, to the problem of finding a needle in a haystack (though he said ‘meadow’). Nearly five hundred years later, whilst still much quoted, it isn’t generally a problem we have anymore. Because we have powerful magnets, in the form of data, algorithms and computers. To find a needle today you need to first hypothesise what type it is, and then decide, and acquire, the data that you can interrogate that will lead to it. A more modern saying comes from Google: ‘in God we trust, everyone else bring data’.

Data is though a troubling mistress: it can represent correlation or causation. Knowing the difference is a skill worth learning and a source of strong competitive advantage. Which is why understanding data is such a key part of any digital strategy.

So how do you use data to boost your business? First off you need to be alert to its importance; once you set your mind to thinking ‘could ABC data help me achieve XYZ outcome’ you will start to be aware of all the data that surrounds your day to day activities. Instead of bemoaning that we are all drowning in data you will start to think of it as fuel, something that can power something else. And as the use of data permeates our lives we are naturally becoming more attuned to what is possible. For example, who doesn’t just ‘look it up on Google’ when they need to know something, or check their train is on time via an app, or order that book that someone is talking about on the radio as you lie on the sofa.

It is data that is removing friction from our lives, enabling us to spend more time doing something than planning to do something. And in a nutshell, for businesses, that is the second point to address; what are our customers after that data could help us provide in a more frictionless way? How do we make this service, product, interaction, building, city smarter? And by smarter we mean more attuned to the needs of the consumer, not the provider. Well today, one of the key ways is through data.

How do you make this happen:

1. Start with an hypothesis. If we knew X would we be able to predict Y? Or rather, could we say Y is 80% likely to occur if X happens? Because computer prediction is actually about probabilities rather than forecasting the future, and whilst not perfect, high probabilities can save you an awful lot of time and money.

So, in the context of real estate, one might ask: ‘when will this homeowner move’, ‘when will this company need a bigger office?’, ‘what asset would this investor buy?’, ‘how much will this building cost to run?’.

2. Once you have your hypothesis you need to define the metrics you would need to answer the question? So you might ask ‘what is the average time someone in that street stays in their home’ or ‘show me every asset that this investor, or investors like them, have bought in the past’ or ‘show me historical costs for a similar building, with similar tenants’.

Nobel Laureate Daniel Kahneman has told us all about ‘Thinking, Fast and Slow’ and the relevance to business is great. Citing real estate again, the industry loves the notion of ‘Fast’ thinking, which is really our instinctive reaction to any situation, our gut if you like. ‘We are a people business’ is symptomatic of ‘Fast’ thinking; through our networks we ‘just know’ the right person for that space, or the perfect investor for that building. Such ‘knowledge’ is indeed a valuable asset, but the future belongs, I think, to more ‘Slow’ thinking. Being asked what is 2+2 is an easy thing for our fast thinking mind to deal with but what is 28,489.2 times 6,870.306 requires the different skill set embodied in our slow thinking mind. In real estate, we need to be looking at how greater use of data, and analysis, can enable us to answer more questions, that are more complicated, and provide answers that are more optimally attuned to real needs, desires and aspirations.

With better data, we can define better metrics, and with better metrics we can do a better job, both for ourselves and our customers. Hunches have their place, but now that we have more data, more sophisticated algorithms, and faster computers, we should be making use of them.

3. Ask the right question, use the right metrics to answer, and you should have an outcome of insights that are valid and verifiable. These of course may well disprove your hypothesis, in which case you can move on to test another. Insights that lead to you not doing something can of course be just as valuable as those that lead to action.

This stage is a prime example of why ‘the robots’ will not take all our jobs, because it is for you to discern whether your insight really is causation, or just correlation. Have you the data you need, and enough of it, to take this answer as final? Do you believe the answer? Does it surprise you?

It is an absolute truth that data is the great enabler of the modern world. Without data all the computational power at our disposal, all the machine and deep learning algorithms at our behest, are worthless. The more you have the better, but there is a big but. It is still our brains that need exercising in asking the right questions, and judging the final validity of what the machines are telling us.

The world is moving from running on oil to running on data, and knowing where data fits in your digital strategy is up near the top of ‘must have’ skills.

Being Digital in Property - Your starter for 10

April 2016

21 years ago I heard MIT’s Media Lab founder Nicholas Negroponte give a lecture on Being Digital. It has taken 21 years, but what seemed obvious then has at last gained general acceptance. Tech is now big, though today you have to call it #PropTech, as if it is something new. and disruptive. It isn’t, and in Property at least, it won’t be.

And it isn’t, and won’t be, because every business is becoming a digital business. Some are taking training steps, whilst others have the gait of a Usain Bolt, but no-one can afford to not move down the digital road. And the great thing is that with 21 years of what the economist Carlota Perez has described as the technological ‘Installation Phase’, we are now moving into the ‘Deployment Phase’. In a nutshell the infrastructure is in place and the world (or at least half of it) are entering a golden age where new technologies are rolled out and capitalised on. So, as long as you don’t shut your eyes and pine for the last golden age, we are all in a position to take advantage of some extraordinary hardware and software.

What?, So What?, Now What?

1. Smartphones. The most important technology the world has ever seen. A market ten times bigger than any other, billions of people worldwide are buying new phones every two years. And every two years they are doubling in capabilities. As Benedict Evans says “The smartphone is the new sun”. More and more your will run your business via your phone, so ensure you have one no more than two years old. And it must be either an Apple iPhone or Android based. Those two operating systems have both won the war, so do not buy a loser.

2. Tablets. The work you do not do on your smartphone you will probably do on a tablet. Yes you will hear people say “But I can’t do real work on that”, but the nature of real work is changing and for perhaps 90% of what needs to be done, a tablet is adequate. They are also fast, light and portable with long battery life. if you are (really) heavy Office users then buy a Surface Pro 4, otherwise either of the iPad Pro’s. These are for work so no cheap copies please.

3. Laptops. Being mobile is the future that is here today. By all means keep your desks with large screens on them, but move to laptops as the default ‘PC’. And seeing as they are substantially cheaper than they were 20 years ago no cheap ones here either.

4. Cloud based software. Whether you are a one man band or multinational, you all have access to the same software, via SaaS (Software as a Service) Cloud apps. Do not buy software you have to load locally or install on your network (as a rule of thumb). Office 365 or Google Apps for Work is foundational, thereafter a CRM, Project and/or Task Manager and Dropbox covers a lot of everyday requirements. Mailchimp is excellent for email marketing. If you need industry specific tools try before you buy. Do not buy anything that is not mobile friendly (this will remove many property software vendors straightaway – good).

5. Broadband. The faster the better. If you can stretch to Gigabit broadband (through the likes of Hyperoptic) buy it; the more you have the more you can do, even if you cannot see what you would use it for today. Ultrafast opens up a hidden world of capabilities (trust me on this).

6. Apps. You will obviously have mobile versions of your core and industry specific apps, but other must haves include the Google set (Search, Maps, Translate, Photos etc), CityMapper and The Trainline for local travel, Slack (end of email?) and LinkedIn for business communication, and then the full range of social media apps. You may think Facebook, Twitter, Instagram, Snapchat and the like are for play, but they are not. Or not exclusively. They are where you will find your customers.

7. Podcasts. More and more industry or domain specific Podcasts are becoming available. There are excellent technology, strategy and management ones as well as an increasingly good one from EG itself. Download a Podcast app, subscribe via iTunes or Google Play and listen to them on the way to and from work.

8. MOOCS. Massive open online courses, from FutureLearn (Open University), Coursera, Stanford, Oxford or many other places are a treasure trove for continuous learning. Often short courses, heavily video based they are perfect for your tablet!

9. Google Squared Digital Marketing Course. Every property company should have at least one member of staff who has done this course, which takes six months and is all online. The Property industry is, by and large, not good at online marketing; this course would help put this right.

10. Books. Yes, paper is allowed, even in a digital company. And there are at least 6 must reads each year. Follow me on Twitter for digitally focussed recommendations.

So 10 practical recommendations for running digital businesses. None are onerous, most are fun, and together they will help keep you beyond the clutches of the #PropTech marauding hordes.