Are you in the wrong half of Real Estate?

The 4-quadrant framework for surviving the hollowing out of the industry’s analytical core.

Last week we covered Pierson Ferdinand: 270 partners, no US associates, AI doing what juniors used to do. That was the firm-structure scale of a dynamic that has been building for two years. This week the capital-deployment scale arrived, and arrived with two frontier AI labs at once. The convergence forces a question on the industry: is real estate still one career? It plainly is not. The bifurcation has begun, and it is going to define the next ten years of who gets paid, who gets promoted, and which firms still exist in 2035.

EXECUTIVE SUMMARY

The first week of May 2026 produced three apparently separate signals: MetaProp Labs released a public catalogue of CRE-specific AI Skills; Anthropic announced an enterprise services firm with Blackstone, Hellman & Friedman and Goldman Sachs; and OpenAI reportedly raised over $4bn for a PE-backed deployment company carrying a reported 17.5% guaranteed annual return for its sponsors. Read together, they describe a single dynamic: AI is industrialising the codifiable, financial-instrument layer of CRE far faster than it is changing the physical-asset layer. This piece offers a two-axis framework: site-specific dependence and named professional accountability. The result is four quadrants with materially different futures. The strategic implication is that single-career framing is now actively misleading. Locating yourself accurately is the precondition for everything else.

THE WEEK THE BIFURCATION BECAME UNMISSABLE

Three things happened, and they look unrelated until you notice they aren’t.

MetaProp Labs published a public catalogue of CRE-specific AI Skills: machine-readable, downloadable, free to install across Claude, ChatGPT, Copilot and Gemini. Deals, asset management, leasing, accounting, legal, investor reporting. It is the public-tier expression of a much larger movement: codifiable industry expertise, packaged for portable consumption, available to anyone with a browser and an API key.

Anthropic announced a new enterprise services firm with Blackstone, Hellman & Friedman, Goldman Sachs and a consortium of further alt-asset managers. The firm will place AI engineers inside portfolio companies to bring Claude into core operations. Blackstone, for the avoidance of doubt, owns more commercial real estate than anyone else on earth.

The same week, OpenAI reportedly raised over $4bn from Brookfield, TPG, Bain and others to launch a competing deployment company, valued at $10bn, majority-owned by OpenAI, with a reported 17.5% guaranteed annual return promised to its private equity backers over five years. If accurate, that detail is the tell. It is a financial-engineering product as much as a technology rollout. The return is not earned on growth. It is earned on compression.

Three artefacts. Three scales: public-tier skills, consortium-tier deployments, capital-tier returns guarantees. One underlying dynamic the industry has not yet named clearly enough.

THE PUZZLE

The intuitive readings are familiar. The optimistic version: AI is industrialising in CRE, the pie is getting bigger, mass-market access to institutional-grade thinking is finally possible. The pessimistic version: the pyramid is breaking, most current jobs disappear, the industry is heading for the same compression as investment banking.

Both readings are incomplete. They share an assumption the events of this week ought to make untenable: that CRE is one industry on one trajectory.

Look at the three artefacts again. The MetaProp Labs catalogue is overwhelmingly aimed at the analytical layer of CRE: deals, asset management, investor reporting, accounting. Pierson Ferdinand is a law firm, a pure financial-instrument-layer professional services business. Blackstone’s deployment of Claude across BREIT, BPP and the European logistics platforms will hit the analytical and investor-reporting layers first, well before it touches a Manchester PRS scheme’s leasing operation or a Birmingham office’s facilities team. The same dynamic that is industrialising on one side of CRE is barely visible on the other.

Real estate has stopped being a single industry on a single trajectory. It is two industries that share a name. The week’s news is the moment that becomes impossible to ignore.

THREE REASONS TO READ THE NEWS CAREFULLY

Before going further, three caveats. None of them changes the structural argument. All of them change how to read the announcements themselves.

First: A press release is not an execution. Enterprise software is full of multi-billion-dollar consortium deployments that produced expensive PowerPoints and not much operational change. The pattern is consistent: capital and brand-name partners assemble around a real bottleneck, eighteen months of building, then collision with the operational reality of getting hundreds of mid-market companies to actually change how they work. Roughly 70% of large-enterprise digital transformation programmes miss their stated objectives, and the most common failure mode is precisely the one this consortium structure produces: capital-and-mandate-driven rollouts pushed down through portfolio companies whose operating teams didn’t ask for the system, don’t trust it, and quietly resist it. CRE operations are particularly exposed because the work is local, embodied, and depends on tacit knowledge that headquarters does not have.

Secondly: The model providers and their customers have inverted incentives. The frontier labs make money when their tools are used more: more tokens, more agents in production, more model calls per workflow. The customer makes money when business outcomes are produced with fewer tokens, smaller models where they suffice, and the minimum viable deployment that delivers the result. A deployment company majority-owned by the model provider, staffed by engineers measured partly on AI consumption, has a structural conflict of interest with the customer’s cost-efficiency goal. Forward-deployed engineers sound like service. They are also a sales channel, and a quiet conduit for everything those engineers see while they are inside your operation. There is more to say about this. It will be the subject of next week’s piece.

Thirdly: There is a financial-engineering smell to all this that will not sit comfortably inside an industry rediscovering itself as operational. Real estate has spent the last five years remembering that it is an operational business: the rise of operating partners over fund managers, the mainstreaming of BTR and life sciences and hospitality-led residential, the shift from spreadsheet returns to building-level performance. An AI deployment story sold by Wall Street, packaged with a guaranteed-return wrapper, marketed through portfolio mandates, is going to land badly with the people who actually run buildings. They are right to be cautious. The framework that follows holds regardless of whether any specific consortium succeeds, because the thing commoditising the codifiable layer of CRE is the model itself, available to anyone with an API key and a SKILL.md file. The consortium is downstream of that.

CODIFIABLE AND ACCOUNTABLE

Some knowledge travels in a SKILL.md file. Some doesn’t. The difference is what is being commoditised this week and what isn’t.

Codifiable knowledge is the kind you can write down as a procedure: comp set construction, T-12 normalisation, cap rate triangulation, debt sizing, lease abstraction, IC memo first drafts, valuation models, variance analysis, lender reporting templates. It travels well. It can be packaged, shared, and run by an AI agent with the right context. The MetaProp Labs catalogue is a public library of exactly this kind of knowledge. The new Anthropic-Blackstone and OpenAI-Brookfield deployment firms exist to industrialise the same kind of knowledge inside large portfolios at speed. Codifiable work is directly substitutable.

Non-codifiable knowledge is what Aristotle called phronesis: practical wisdom built case by case, mistake by mistake, consequence by consequence. The investor who senses a deal start to break in a way the spreadsheet does not yet show. The planning consultant who knows which conservation officer in which authority will sympathise with massing exceptions. The retrofit coordinator who knows which contractor on her list can actually deliver the airtightness numbers the model assumes.

Phronesis is not magic, and it is not immune to AI. It is formed through consequence. It comes from seeing real buildings, real tenants, real contractors, real planning committees, real lenders and real mistakes. AI can support this work, document it, search precedent around it, and remove much of the administrative drag. What AI cannot do is become the named person who has lived through enough cases to know when the written procedure is about to fail. Non-codifiable work is indirectly leveraged by AI: the administrative layers around it get stripped away, output rises, and the burden of named accountability sits on fewer humans, more squarely. That accountability becomes scarcer because output is increasing faster than trusted sign-off.

The asymmetry between these two kinds of knowledge is the engine of the bifurcation. Direct substitution on one side, indirect leverage on the other. Where a CRE role sits on that spectrum determines almost everything about its trajectory.

GOOD, BETTER, BEST

Skills, using Anthropic’s Agent Skills methodology, can be deployed at three tiers, and each tier compresses a different layer of work at a different speed.

Good is the public, free, generic skill. The MetaProp Labs catalogue. A SKILL.md file you download and install, designed to work on standard inputs with institutional-standard procedure. It gets a small landlord 80% of the way to institutional-grade thinking on a routine task. Genuinely valuable, historically unavailable. Compresses the floor of the analytical pyramid first and most violently.

Better is the private, firm-tuned skill. The same procedural backbone adapted to a specific firm’s data, conventions, templates, and house view. Built and maintained internally by someone who owns it as an asset. Compresses analyst headcount by 60-80% on the tasks it covers, and creates one new role: the person who builds, curates and improves the skill library. This tier is where mid-tier firms either build a moat or fail to.

Best is the engineered, agentic, system-level deployment. Skills composed into orchestrated workflows with memory, evaluation harnesses, monitoring, exception handling, sub-agents and feedback loops, integrated with the firm’s data substrate, observable enough to be trusted with consequential decisions. This is what the new Anthropic and OpenAI services firms have just been capitalised to build. It is, in practical terms, a moat for the largest sponsors, and a serious build problem for the operationally disciplined mid-tier firms that prefer to construct their own version internally rather than rent it from a consortium.

Three tiers. Different costs, different defensibility, different effects on different parts of the industry.

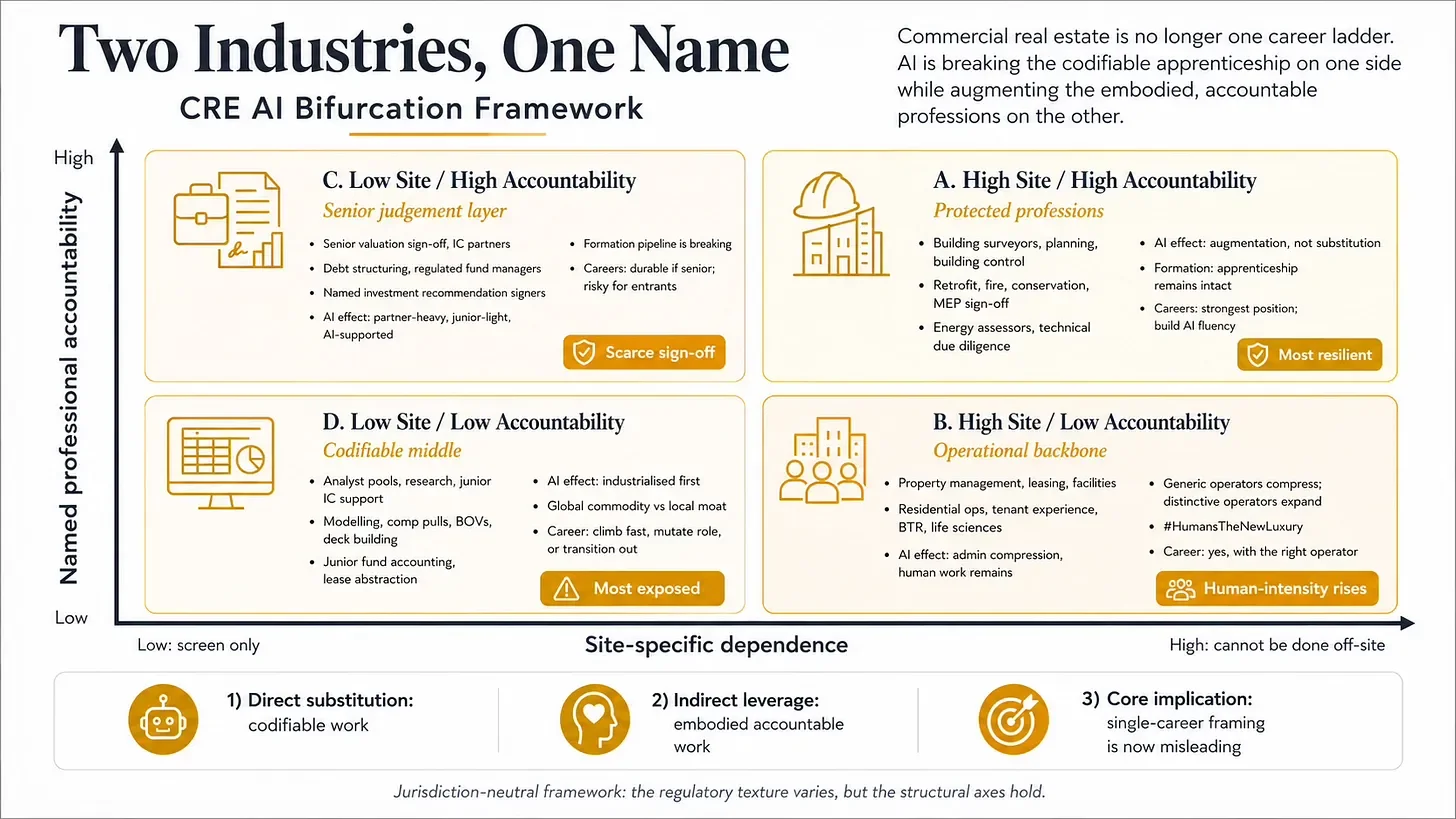

THE TWO AXES

The framework rests on two axes. Both are jurisdiction-neutral, although the regulatory texture varies: RICS in the UK, the appraisal regime in the US, Sachverständigenwesen in Germany, expert agréé in France. The structural axes hold regardless.

Axis 1: site-specific dependence. How much does the work depend on local, physical, asset-level, tenant-level or regulatory context that cannot be fully reduced to a document set? The answer ranges from “screen only” to “cannot be done off-site”.

Axis 2: named professional accountability. How much of the role’s value comes from a human or institution putting their name, licence, indemnity, balance sheet or regulatory standing behind the answer?

Two axes. Four quadrants. The bifurcation runs through them.

QUADRANT A: HIGH SITE, HIGH ACCOUNTABILITY

Building surveyors, planning consultants, building control, retrofit coordinators, fire engineers, conservation architects, MEP engineers with statutory sign-off, certified energy assessors, technical due diligence professionals. The protected professions of CRE, where the work is anchored to a specific building, a specific authority, and a specific named person who has to stand behind the answer.

This quadrant is the most resilient of the four, and arguably the strongest position in the entire industry. Demand is growing, driven by the largest infrastructure programme in human history: the decarbonisation of the built environment. The UK alone needs to retrofit 28 million homes and over a million commercial buildings to net zero by 2050. Add building safety remediation post-Grenfell, the conversion of redundant office stock to residential, the planning system’s chronic understaffing, the AI data-centre and logistics build-out, the housing crisis. None of this is being automated away.

The formation pipeline in this quadrant is also intact, almost by accident. A young surveyor learns by walking buildings with a senior surveyor. A planning consultant learns by sitting in committee meetings. The apprenticeship is embedded in physical work that AI does not displace, which means phronesis still develops through the channels that have always developed it. AI shows up here as augmentation: better measurement, faster reporting, fewer errors on routine paperwork. The role gets more leveraged. Viability stays.

Career advice for this quadrant: yes, with confidence. Build AI fluency to multiply your output, but do not mistake the AI for the job. The job is still the building, the local context, the regulation, and the named responsibility you sign your name to.

QUADRANT B: HIGH SITE, LOW ACCOUNTABILITY

Property managers, leasing agents, facilities managers, project managers below sign-off level, residential operators, hospitality-led workplace teams, tenant experience leads, asset operators in BTR, life sciences and logistics. The operational backbone of the industry.

This quadrant is resilient but compressing in its administrative layer. AI takes the paperwork fast: lease renewal correspondence, work-order triage, basic tenant queries, scheduling, rent collection chasing, comp gathering. What it leaves alone is the relational, operational, and physical work: walking the asset, talking to the tenant, supervising the contractor, negotiating with the local authority, handling the moment when something goes wrong at 2am. The role gets redefined toward the human-intensity end.

This is where the asymmetric outcome lives. Generic property management businesses compress. Operationally distinctive landlords expand. #HumanIsTheNewLuxury was always pointing here. Hospitality-grade residential, life sciences operations, experiential retail, members’ clubs, curated workplace: these buildings need more people per square foot than today’s mass-market institutional landlords employ, because the per-asset relational density is higher.

Career advice for this quadrant: yes, with the right operator. The serious operational landlords of the next decade win. Generic property management businesses lose. Pick carefully.

QUADRANT C: LOW SITE, HIGH ACCOUNTABILITY

Senior valuation partners signing for secured lending and fund reporting, IC partners with named responsibility, debt structuring at partner level, fund managers with regulatory accountability, named investment recommendation signers, partners signing audited reports. The senior judgement layer of the financial-instrument business.

This is the Pierson Ferdinand quadrant for CRE: partner-heavy, junior-light, AI-supported. Resilient at the top, compressing in the middle, breaking at the bottom. The senior roles survive because the legal and regulatory structures of the industry require named human accountability. As AI floods the world with analytical output, the scarce resource becomes the qualified human willing to take fiduciary responsibility for the answer. That role gets more valuable in the short run.

But the formation pipeline is breaking. The seniors of 2040 were supposed to be formed through the analytical apprenticeship that produced today’s seniors: ten years of comps, models, memos, IC support, supervised exposure to consequential decisions. AI is hollowing out exactly that apprenticeship faster than firms have built a replacement for it. Pierson Ferdinand has decided, openly, that someone else will train the lawyers it eventually hires. Most firms quietly cutting graduate intake and slowing trainee programmes are echoing the same choice without naming it.

Career advice: yes if you are already senior, very risky if you are trying to enter via the traditional pyramid. The traditional pyramid no longer reliably leads to seniority because the rungs have been removed. Entrants need to find one of the firms consciously over-investing in formation against the sector trend, or build seniority through an unconventional path: founder roles, specialist boutiques, family offices, in-house at a sophisticated owner-operator. The era of “join a big house, learn the trade, make partner in twelve years” is closing on this quadrant. It hasn’t fully closed. It is closing fast.

QUADRANT D: LOW SITE, LOW ACCOUNTABILITY

Analyst pools, research, junior IC support, model maintenance, comp pulls, BOV production, deck building, capital markets junior tiers, junior asset management analytics, lease abstraction, draft variance commentary, junior fund accounting, junior valuation modelling. The codifiable middle of the financial-instrument layer.

This is where the pyramid is breaking fastest and most visibly. The MetaProp Labs catalogue is principally aimed here. The new deployment firms are designed to industrialise here. Brynjolfsson, Chandar and Chen at Stanford’s Digital Economy Lab found a 16% relative employment decline for workers aged 22-25 in AI-exposed occupations through 2025, with wages in those roles actually rising. Fewer, more experienced workers doing more. This is not CRE-specific evidence, but it describes exactly the labour-market pattern one would expect if codifiable entry-level cognitive work is being automated first.

There is also a geography to this. Quadrant A is a local moat: the building stays, the planning officer stays, the regulatory regime stays, and the value sits in the named professional embedded in that local market. Quadrant D is a global commodity: a junior CRE analyst’s work is now competing in a global labour market that includes Mumbai, Manila, and any AI agent with an API key. The bifurcation is therefore also a geographic asymmetry. A is locally protected. D is globally exposed.

The career question follows directly. There is no stable long-run position in Quadrant D doing the work as currently structured. Three to five years is the maximum viable time at this altitude before the role’s value has fully migrated to the agents performing it. Drifting in Quadrant D means waking up at 35 with a CV full of work that an agent now does cheaply, instantly, and well enough.

But the quadrant offers three constructive paths out, and the framework should name them clearly.

The first is accountable judgement: build the AI fluency, the relationships, and the domain depth to break into Quadrant C before the formation pipeline closes. The traditional path, now compressed into a shorter window than it was for previous generations, but still real for those who move fast.

The second is relationship-led origination: reposition toward the parts of the financial-instrument layer where the work is fundamentally about sourcing, trust, and client relationships rather than analytical production. Capital raising, deal origination, investor relations, specialist brokerage. These roles sit nominally in low-site territory but are protected by the relational density AI cannot replicate.

The third is AI-enabled workflow ownership: move up the stack from producer to architect. Stop being the person who writes the lease abstract or the BOV; become the person who designs, curates, and continuously improves the firm’s internal skill library, eval sets, monitoring systems, and orchestrated workflows. This is the betterand best tiers of the good/better/best ladder applied inside your own firm. It depends on deep tacit knowledge of how this firm - its data, its templates, its edge cases, its house view - actually operates. That tacit knowledge is its own kind of non-codifiability. It is also, not coincidentally, exactly the work that RIRA’s verifiable cognition layer points toward, and one of the few genuinely scarce roles AI is creating rather than destroying. It deserves more weight than this framework can give it in passing. We will return to it next week.

The framework’s instruction to Quadrant D is therefore not “transition out”. It is “move up, sideways, or up the stack - but do not stay still”. Drifting is the only path with no future.

THE TAM ARITHMETIC

A counter-argument to all of the above is the one a thoughtful reader will raise here: even if the per-role labour content collapses, the market for CRE services is going to expand by 10x as AI brings white-glove services to mass-market clients. Total industry employment grows. The displacement is real but absorbed.

The argument is partially right and substantively wrong. A stylised example makes the point.

Imagine a UK retrofit advisory market with 2,000 specialists today, serving 10,000 assets a year at five-figure fees. Tomorrow, AI-enabled mass-market retrofit advisory could serve a million assets a year at three-figure fees. The market expands by 100x. But the labour intensity per asset has collapsed. If the mass-market service requires one human per 2,000 clients (because most of it is automated), that’s 500 humans serving the million assets. Total advisor headcount: a quarter of what it was. Total market revenue: meaningfully larger.

The pie expanded. The headcount that serves the pie shrank. This pattern shows up in robo-advisory in wealth management, in Squarespace versus the bespoke web design industry, in TurboTax versus high-street tax preparers. Total category spend rose. Total category employment fell.

Worse, the new TAM is rarely captured by the firms that currently serve the old TAM. The mass-market version of strategic asset management for small landlords will not be sold by JLL. It will be sold by a PropTech platform, possibly one that does not yet exist, with a payroll a fraction of the incumbents whose work it commoditises. TAM expansion is real. It does not automatically rescue the incumbent labour model. In most technology transitions, the new demand is captured by new operating models, new distribution channels, and much smaller teams.

The bigger pie is real. It is not the same as more jobs.

WHAT THIS MEANS FOR YOU

Locate yourself accurately on the two axes. Do not guess. Do not be optimistic.

If you are in Quadrant A (surveying, planning, retrofit, building safety, fire engineering, technical due diligence), you are in the strongest position in the industry. Build AI fluency to multiply your output, deepen your local market knowledge, and recognise that what you have is structurally valuable in a way most of your colleagues in other quadrants do not. Do not waste this position by treating it as ordinary.

If you are in Quadrant B (operational asset management, leasing, facilities, residential operations, hospitality-led workplace), pick your operator carefully. The serious operational landlords of the next decade will employ more people per square foot than today’s mass-market institutional ones do, because the per-asset relational density is higher. Generic property management businesses will compress. Operationally distinctive ones will grow.

If you are in Quadrant C (senior fiduciary roles in the financial-instrument layer), your individual role is durable for a decade or more. The problem is what comes next behind you, and whether your firm is doing anything serious about formation. Ask the question. If the answer is “we have outsourced training to AI”, you are working in a firm that is harvesting the last generation of seniors and not replacing it.

If you are in Quadrant D (analyst pools, junior research, model maintenance, deck building), you have a planning horizon of three to five years for the work as currently structured. Three real options: climb into Quadrant C, reposition into Quadrant A or B, or move up the stack into AI-enabled workflow ownership inside your current firm. The longer you drift without choosing one, the harder all three become.

WHAT THIS MEANS FOR FIRMS

The framework changes how a firm should think about itself, particularly if it operates across multiple quadrants. Most large CRE firms do.

The same firm cannot run a single formation model across all four quadrants. A firm with a Quadrant A surveying business and a Quadrant C investment business is, in capability development terms, two firms in one suit. The surveying business should keep training the way it has always trained: real buildings, supervised work, deliberate exposure to the kind of mistakes that build judgement. The investment business needs an explicit redesign of its formation pipeline because the apprenticeship that used to produce its seniors is gone. Treating them as one career path was always a polite fiction. It is now a strategic vulnerability.

Firms straddling Quadrants C and D have a particular problem and a particular opportunity. The problem: the C quadrant depends on a junior pipeline that the D quadrant is industrialising out of existence. The opportunity: cross-subsidising deliberate phronesis development from the firm’s other revenue lines may be one of the few defensible moats in a world where the codifiable analytical layer is commoditised. Pierson Ferdinand has chosen the opposite strategy. Quietly, most large firms are also choosing it without naming the choice. The firms that consciously do the opposite, that over-invest in formation, will produce the seniors of 2040, and will be paid premium prices to provide them to the firms that did not.

Build versus buy on AI deployment is also an open question, and the consortium narrative is trying to close it prematurely. My hypothesis: the operationally disciplined mid-tier players who build their own better-tier capability incrementally, around their own data, with their own engineers, without the financial-engineering overhead and without the model-provider conflict of interest, will compound advantages that the consortium-led buyers will struggle to match. That is a hypothesis. The next 24 months will test it.

The firms that take this path will need the people described in Quadrant D's third option to do the work. Both halves of the prescription are the same prescription, seen from opposite ends of the org chart.

WHAT THIS MEANS FOR THE INDUSTRY

The bifurcation needs to be named. The single-career, single-firm-strategy, single-industry framing currently dominant in CRE commentary is leading people into wrong quadrants by accident. Smart juniors are walking into Quadrant D because that’s where the entry-level jobs are visible, without understanding the floor is dropping. Mid-career professionals are betting on relational-sector expansion to absorb their displacement, without understanding the expansion will be captured by a different category of firm than the one they work in. Firms are running formation programmes designed for an undifferentiated career path that no longer exists.

This is also a policy and institutional question, not just a firm-level one. The IPF, INREV, ULI, BBP, RICS, RIBA, BCO have all set industry conventions before; they could set capability-development conventions now. A modern guild for AI-fluent retrofit professionals, or for phronesis-development in the financial-instrument layer, would be more useful to the next generation than another conference programme. There is more to say about institutional response and state policy, and it deserves its own piece. For now, it is enough to say the collective-action problem is real, the voluntary bodies are well-suited to address it, and most of them are not yet trying.

THE CHOICE

Two industries. One name.

The events of the past week made the split visible at three scales: public CRE skills at the catalogue level, consortium-tier deployment companies at the enterprise level, and a 17.5% return guarantee at the capital level. AI is not hitting the whole industry equally. It is breaking the codifiable apprenticeship on one side of CRE while augmenting the embodied, accountable professions on the other.

So the important career question is now this. Which part of real estate are you actually in?

If your work is codifiable, low-accountability and far from the asset, the floor is dropping. If your work is site-specific, relational, regulated or consequence-bearing, the tools are getting better and your leverage is rising.

The dangerous answer is the comfortable one: “I work in commercial real estate.” That is no longer specific enough.