The best new PropTech is a CRE company

Fifteen years of 'buy don't build' was the right answer. AI has flipped it.

Fifteen years of ‘buy don’t build’ was the right answer. AI has flipped it. The most consequential new property technology of the next five years will be built inside the firms that need it, not sold to them.

I have written about PropTech, and argued with PropTech founders, for three decades. The assumption underneath the whole industry has been that CRE firms need technology, but cannot build it. That assumption is structurally breaking, and not for the reason most commentators are reaching for. The cause is more interesting than build cost alone: the ‘firm’ itself is becoming something different, and the people inside it are becoming something different. What follows is what that means for which PropTechs survive, and for what your firm should be doing inside its own walls.

Executive summary

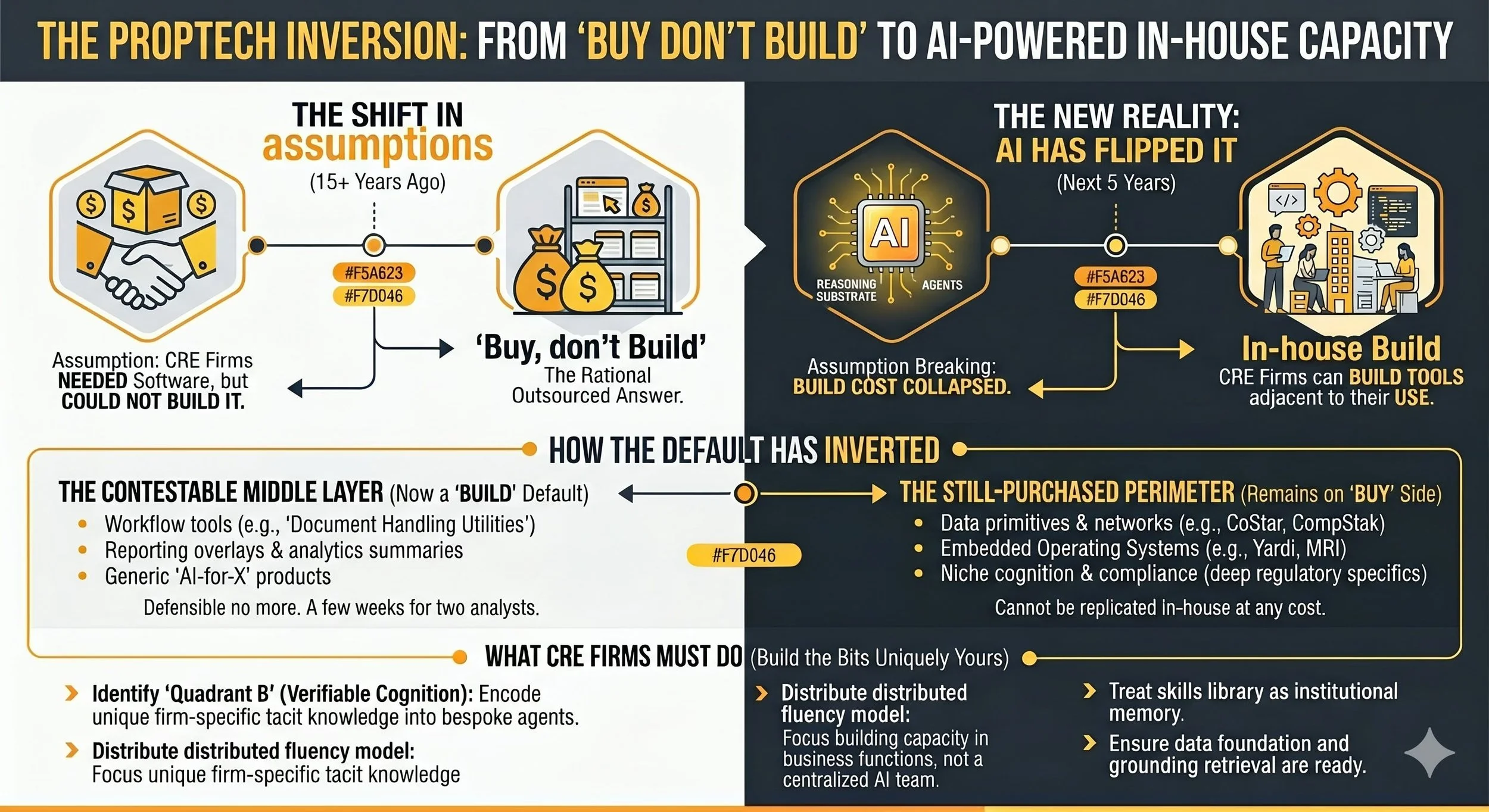

The PropTech industry has spent fifteen+ years on one assumption: CRE firms needed software they could not build themselves. That assumption is now breaking. Build cost has collapsed for domain experts who hold the relevant knowledge, and the working life of the typical CRE professional is reshaping around agent orchestration in a way that makes building feel adjacent to using. Together those two shifts have inverted the ‘buy don’t build’ default. The middle layer of PropTech, the workflow tools and reporting overlays and generic AI-for-X products, is now contestable from inside the buyer. Data networks, embedded operating systems and deeply specialised regulatory tools remain on the buy side. PropTech founders need archetypes that survive this shift; CRE firms need to recognise that their next competitor for cognitive workflows is increasingly themselves.

WHAT HAS ACTUALLY CHANGED

The argument rests on two things happening at once. They reinforce each other, but they need to be seen separately to be understood properly.

The build cost has collapsed

A senior surveyor with access to a properly configured reasoning substrate, a small library of firm-specific skills, and an afternoon free can now produce working tooling that a Series A PropTech would have needed eighteen months and three engineers to ship. Run a ‘Layer 1’ deployment inside most firms that have done the data work, and the demonstration sits on a desktop within days or a few weeks.

That collapse changes the economics of in-house build in a way the industry has not yet absorbed. The old buy-versus-build calculation assumed building required engineers the firm did not have, infrastructure it did not run, and time it could not afford. All three lines have shifted. Two of them have shifted profoundly. The CRE firm that runs the numbers today reaches a different answer than it did in 2020.

That is the supply-side change. It is real and increasingly understood.

The firm is becoming something different

The more interesting change is what the firm itself is becoming, and how that affects who can build what.

Over the next three to five years, the working life of the typical CRE professional will reshape around agent orchestration. The substance of their job, not a layer on top of it. The discipline is curation. The day’s work is orchestration. Scope the task, configure the agent, validate the output, decide what to do with it. That is a different kind of professional, doing a different kind of work, embedded inside a different kind of firm.

Which matters for the buy-versus-build question. The muscle memory of curating an agent is adjacent to the muscle memory of building one. The capability ladder has fewer rungs than it used to. Curating output is the entry-level discipline. Codifying workflow is the next. Building internal tooling is the next after that. Each rung is a smaller step than it was, and the people climbing them are already on payroll.

What this means in practice is straightforward and largely unannounced. Knowledge workers are beginning to build their own software. Not full enterprise systems. Not the platforms procurement signs annual licences for. The specific cognitive tools they need to do their work better tomorrow than they did today. A property lawyer encoding her firm’s approach to lease abstraction as a skill. An asset manager configuring a covenant-watch coworker that flags exposure shifts across the portfolio. A development director building an agent that runs first-pass appraisals against the firm’s house assumptions. None of them call this ‘building software’. They are.

The same shift is visible in the startup ecosystem. The domain expert who used to need a technical co-founder, a contract dev shop, or eighteen months of runway can now be the hybrid technical founder. The surveyor who knows exactly why ARGUS produces unreliable reversionary valuations in a rising yield environment can build directly against that problem. The fund manager who has watched three IC processes fail at the same point can build the fix herself. Both phenomena have the same cause. Both have the same consequence for the buy-versus-build question.

This is the organisational shift that makes the inversion structural rather than situational. The professional class in CRE is not being replaced by AI. It is being restructured around it. That restructuring is the precondition for in-house build to feel natural rather than foreign.

One caveat worth holding in mind. This describes firms that have done the organisational work to support agent orchestration. Most have not yet. For firms still running on conventional structures, deploying AI on top produces automated dysfunction at machine speed, not compounding capability. The thesis applies most strongly to firms that have crossed the organisational threshold, less to those that have not, and not at all to firms that refuse to. The middle layer of PropTech does not die uniformly. It dies at the frontier first, with the customers vendors most need to retain.

For commercial real estate, this restructuring maps directly onto Quadrant B (see previous newsletters) of the CRE Automation Matrix: ‘verifiable cognition’, where firm-specific tacit knowledge gets encoded into firm-specific agents that handle the high-value cognitive work the firm actually does. Quadrant B is where the durable differentiation lives, because the knowledge being encoded is yours and not your competitor’s.

It is also where the buy-versus-build calculus tilts most sharply toward build. The value of Quadrant B work is precisely what makes it un-standardisable. Any vehicle that promises Quadrant B at scale will, by its economics, push toward generalised patterns that work across many firms. The patterns that work specifically for you have to be built by people who know what ‘specifically for you’ actually means. Mostly that is you.

One further dependency. Quadrant B sits on top of the lower layers of the stack. The data foundation has to be reasonable. The reasoning substrate has to be deployed. Grounded retrieval has to be working over firm data. None of that is exotic in 2026, and none of it is free either. The firm that wants to do meaningful Quadrant B work in-house needs to be comfortable with most of the layer cake, not just the top tier. The full architectural argument is in *CRE AI Is a Layer Cake*. The short version: sequencing matters, and the firms that try to start at Quadrant B without the lower layers in place produce the productivity theatre they were trying to avoid.

WHO MAINTAINS WHAT

The obvious objection to the argument so far. Prototypes are cheap. Enterprise capabilities are not. Maintenance, governance, audit, security, integration. None of these has been collapsed by AI to anywhere near the degree first build has. Anyone who pretends otherwise has not actually shipped software inside a regulated firm.

This is half right. The objection assumes the in-house build resembles the old in-house software project: bespoke infrastructure, custom code, internal devops, full-stack ownership. That is not what serious firms are building.

What they are building sits in the upper layers of the stack, on top of platforms the model providers maintain. Configured agents. Skills libraries. Projects. Grounded retrieval over firm data. The model, the orchestration, the security baseline, the inference reliability. All of those are maintained by the platform, not by the firm. The firm maintains the configuration, the prompts, the data connections, the access controls, and the management structure that curates the lot.

The shape of that management structure matters more than most operators realise. The firms doing this well will have built a distributed fluency model: domain experts as builders inside business functions rather than seconded to a central AI team, stewards governing a skills library treated as institutional memory, evaluation infrastructure detecting drift before it bites. The talent-dependency problem of ‘one analyst built it, nobody understands it after she leaves’ is real for firms that have not done this organisational work. It is largely engineered out for the firms that have.

That is a different maintenance problem to the one PropTech sales teams have spent fifteen years warning operators about. The cost is real. The shape is manageable. Any firm that can run a quality management system for its asset data can run one for its skills library and its agent configurations. Where deeper maintenance is genuinely required (bespoke integrations, regulated workflows with full audit chains, mission-critical systems), you bring in partners who manage those workloads professionally. The same way you bring in audit, legal or quantity surveying for the work you do not staff internally.

What you do not do is build random demo-quality apps and pretend they are enterprise systems. That route was always a bad idea and it still is. The category of build worth doing is the category that lives in your firm’s distinctive judgement and benefits from compounding inside the firm. Quadrant B work. Not everything. Not infrastructure. Not commodity workflows. The cognitive workflows where the value sits in your house view of the world.

AI has not made governance optional. It has made ownership newly plausible.

THE INVERSION

The default has flipped.

For fifteen+ years, the right answer to a CRE technology question was almost always ‘buy, not build’. The reasoning was solid. Building required engineers the firm did not have, infrastructure the firm did not run, and time the firm could not afford. The PropTech industry was the rational outsourced answer to a problem the industry was not equipped to solve internally.

That answer was right. It is no longer right for a meaningful slice of what PropTech used to sell.

The slice that has flipped is the middle. Workflow tools that automate cognitive labour. Reporting and dashboard products. Analytics overlays that summarise what other systems already hold. Document-handling utilities, IM drafting accelerators, lease review tools, and most of what is currently described in pitch decks as ‘AI for [X workflow]’. These products were defensible when the alternative was a serious in-house dev project running into years. They are increasingly indefensible when the alternative is two analysts, a Claude subscription, and a fortnight.

The default has not flipped everywhere. Three categories remain firmly on the buy side. Data primitives and networks (CoStar, CompStak, the major brokerage networks) cannot be replicated in-house at any cost, because the moat is contributed data the firm does not own. Embedded operating systems (Yardi, MRI, RealPage, ARGUS) carry years of accumulated process logic, regulatory certifications and integration depth that no internal team can recreate inside a sensible budget. Niche cognition tools with deep regulatory specificity (UK SDLT optimisation, US 1031 exchanges, German Wohnen rules, BNG tracking) live in markets too narrow and too specialised for any single firm to justify in-house work, and the specialist who serves the whole market amortises the rule library across all of them.

Outside those three categories, the default has moved. The answer is now ‘build the bits that are uniquely yours; buy the bits that aren’t’, and the boundary has shifted to give ‘uniquely yours’ a much larger surface area than it had five years ago.

This sounds like a small adjustment, but in reality it is a structural one. The PropTech industry was built around an assumption that the buyer could not be the builder. For the next five years, the buyer increasingly is the builder. The competition for most middle-layer PropTech is no longer another PropTech start-up. It is the CRE firm’s own internal capability, supplied by people who already work there.

Both sides of the market have to absorb this.

WHAT SURVIVES

The inversion clarifies rather than kills PropTech.

What remains genuinely defensible falls into four archetypes. Three exist outside the inversion entirely. The data, infrastructure and specialist categories no in-house build can replace. The fourth is the shape new PropTech takes when the inversion lands: operator-built tools that get spun out.

1. Data primitives and networks

Multi-sided businesses where the moat is contributed or observed data that no single participant could assemble alone. CoStar, CompStak, MSCI/RCA, the major brokerage transaction networks. AI makes genuine network-contributed data more valuable, not less, because it becomes the structured ground truth every AI agent in the industry consumes. However, the category is narrower than the named brands suggest. Data that was merely hard to assemble, involving proprietary scraping, manual research teams, ops you used to need scale to fund, is now increasingly easy to reconstruct. Some businesses currently classed as data primitives sit on the weaker side of that line.

2. Embedded operating systems

Yardi, MRI, RealPage, ARGUS, Tramps, Qube. Workflow lock-in across years, regulatory certifications, complex switching projects, integration depth no internal team can recreate. AI strengthens the incumbents who layer it on top of their existing footprint, because the existing footprint is the asset.

A frontal AI-first challenger PMS is unlikely to win. However, an agent-native operating layer that starts at a specific incumbent failure point, captures workflow-specific data, and gradually becomes the system of intelligence above the system of record is a different proposition, and remains plausible. Particularly in various niches. Mid-market BTR. European multifamily compliance. Single-jurisdiction lender reporting nobody serves well. The lateral entry, not the frontal attack.

3. Niche cognition and compliance tools

The regulatory and structural complexity that generalist AI gets systematically wrong, and that no single firm can justify tracking in-house. UK SDLT optimisation for cross-border investors, German Wohnen rules, US 1031 exchanges and LIHTC modelling, MEES compliance, the UK service charge code, biodiversity net gain, embodied carbon under RICS WLCA, SFDR and EU Taxonomy reporting.

The moat is two-sided: deep edge-cases a generalist team would get wrong, and a moving regulatory target the specialist amortises across hundreds of customers. Ideally founded by a domain expert who personally encountered the problem and now codifies it. The CRE firm trying to track this in-house discovers what ‘compliance debt’ looks like.

This category sits firmly on the buy side. The specialists who serve the whole market amortise the rule library and the regulatory tracking. You would not.

4. Operator-built tools that get spun out

The route to market that probably defines the next five years. Tools built inside major CRE firms (Blackstone, Brookfield, Hines, Greystar, Landsec, and their equivalents) for their own use, validated against billions of AUM, then spun out as commercial products. Operator credibility. Workflow validation against assets that actually exist. Pre-built distribution through the originating firm’s network.

Spinouts work best when distribution is non-competing: a different asset class, geography, or market segment from the originating firm. Vicinitee, which I founded and co-developed with British Land and which Equiem later acquired, ran on exactly that logic. Most of the credible new PropTech I expect to emerge between now and 2030 will come through this path, rather than through VC-backed SaaS founded outside the industry.

The pattern underneath the four

The four archetypes share a test. The PropTech that survives is the kind an incumbent cannot easily extend into, an in-house team cannot easily build, and a generalist AI cannot easily replicate.Most of these pass two. The best pass all three. Anything that fails all three is exposed, regardless of pitch deck or capital raised.

For a tech founder, the archetype tells you whether the idea has a future. For a CRE firm, it tells you what is still worth buying, and what to start building.

HOW INCUMBENTS GET OUTMANOEUVRED

The first two archetypes look unassailable. Data primitives like CoStar and embedded operating systems like Yardi have spent decades accumulating moats that no challenger can match head-on. The conventional wisdom says do not attack them, route around them.

The conventional wisdom is right. There are three credible ways through.

1. The over-the-top intelligence layer

Features accelerate a step in an existing workflow. Agents own the workflow and make the step structure obsolete. That distinction matters most where the workflow lives across multiple incumbent systems.

The CRE technology stack is a mess. Yardi, MRI, RealPage, ARGUS, CoStar, and dozens of point solutions. Each holds part of the picture. None can credibly offer the integrated reasoning layer above the lot, because each has an interest in privileging its own data. A vendor whose business model depends on its ecosystem cannot honestly treat its own data as one input among many.

That structural conflict is the opening. An intelligence layer that ingests data across legacy systems, resolves their inconsistencies, and provides unified reasoning is something the incumbents cannot match without cannibalising their own subscription revenue. The reader who has watched a quarterly portfolio review knows the operational gap intimately. The data lives in seven systems. The decision needs all seven.

There is a caveat worth flagging. MCP and standardised agent protocols are compressing the integration work this play depends on. The intelligence layer was a moat in 2024 because connecting systems was hard. It is increasingly available as infrastructure rather than as a defensible product. The play still works, but more as a capability CRE firms build for themselves than as a venture-scale category. The buyer-is-the-builder logic of this whole piece bites here too.

2. Attacking specific incumbent failure points

Frontal attacks on embedded operating systems are nearly dead. Lateral entries are not. The incumbents have structural blind spots, and challengers who concentrate on a single underserved segment can build credible positions before the incumbent notices or chooses to respond.

Mid-market BTR. European multifamily compliance. Single-jurisdiction lender reporting nobody bothers to do well. Niche operator categories where the incumbent product is genuinely poor, the customer base too small to interest the incumbent but too important to leave underserved. The play works because the incumbent’s economics push it toward broad horizontal capability, not toward deep vertical excellence. The gap is permanent. The opportunity is not.

3. Services-as-software

The most underappreciated of the three. Buyers do not want software. They want the work done. The traditional PropTech model sold a tool that helped a customer do work. The services-as-software model sells the completed work itself, with AI doing the heavy lifting inside the vendor.

The customer receives the maintained compliance evidence file, the lender reporting pack, the rent reconciliation, the planning submission draft. The customer sees outcomes, never software. The vendor takes the professional risk and prices the output rather than the seat. The model bypasses incumbent OS systems entirely. It competes for the result rather than the workflow.

The reason this is durable in CRE specifically: most of the high-value work is regulated, professional, and accountability-bearing. AI can do the cognitive labour, but somebody has to sign off. A services-as-software vendor that takes that liability captures margin no SaaS product could justify. The closest analogy outside CRE is the rise of in-house legal teams backed by AI-augmented external counsel: clients pay for the outcome and the accountability, not the tool that produced them.

What the three share

Each play routes around the incumbent’s strength by attacking from a direction the incumbent cannot credibly defend. The over-the-top layer attacks the closed ecosystem with openness. The failure-point play attacks horizontal breadth with vertical depth. Services-as-software attacks workflow ownership with outcome ownership. Each is a route through territory the incumbent built without considering this kind of competition could exist. AI is what makes all three economic. The incumbent has the data and the workflow. The challenger now has the cognition.

SO WHAT NOW

If you are running a PropTech, the question is whether your archetype is in the four. If it is, the question is whether you pass at least two of the three tests. If it is not, the question is how quickly you can move into one that is. The conventional answer is to raise more capital and grow into defensibility. The current answer is that capital does not buy you past any of the three tests. Adding scale to a category the inversion has hollowed out is a more expensive way to discover you have built the wrong thing.

If you are running a CRE firm, the question is which of your differentiating workflows you have allowed to live inside a vendor’s product. The default has moved. The vendor lock-in you have been managing was the right risk to take in 2018. It is the wrong risk to be carrying in 2027. The work of pulling Quadrant B back inside the firm is unglamorous, slow, and unavoidable. It also compounds. Buying rarely does, in the workflows where your judgement is the asset.

There is a larger question the industry has not started asking out loud. The PropTech category was built around venture capital and the assumption that scale follows product. If most of the surviving archetypes are not venture-scale, what happens to the category as a category? My current view is that PropTech contracts as a separate VC asset class over the next five years, and value capture migrates from venture investors back into the operator firms that now have the means to build for themselves. The category does not disappear. It gets absorbed.

The best new PropTech is a CRE company. Sometimes this is a literal claim about a tool spun out of a real estate firm with a £20bn portfolio behind it. More often it is the smaller claim that the most consequential property technology of the next five years was built inside the firm that needed it, by people who already worked there, and never reached the market at all.

For fifteen years, the smart firms bought what they could not build. For the next five, the smart firms will build what others would have sold them. The firms that see this first will spend the time quietly compounding the capability that the rest of the industry will eventually have to procure from someone.

Probably them.