CRE: Constraints, Moats and Value

AI is removing the constraints that built CRE’s moats. What replaces them?

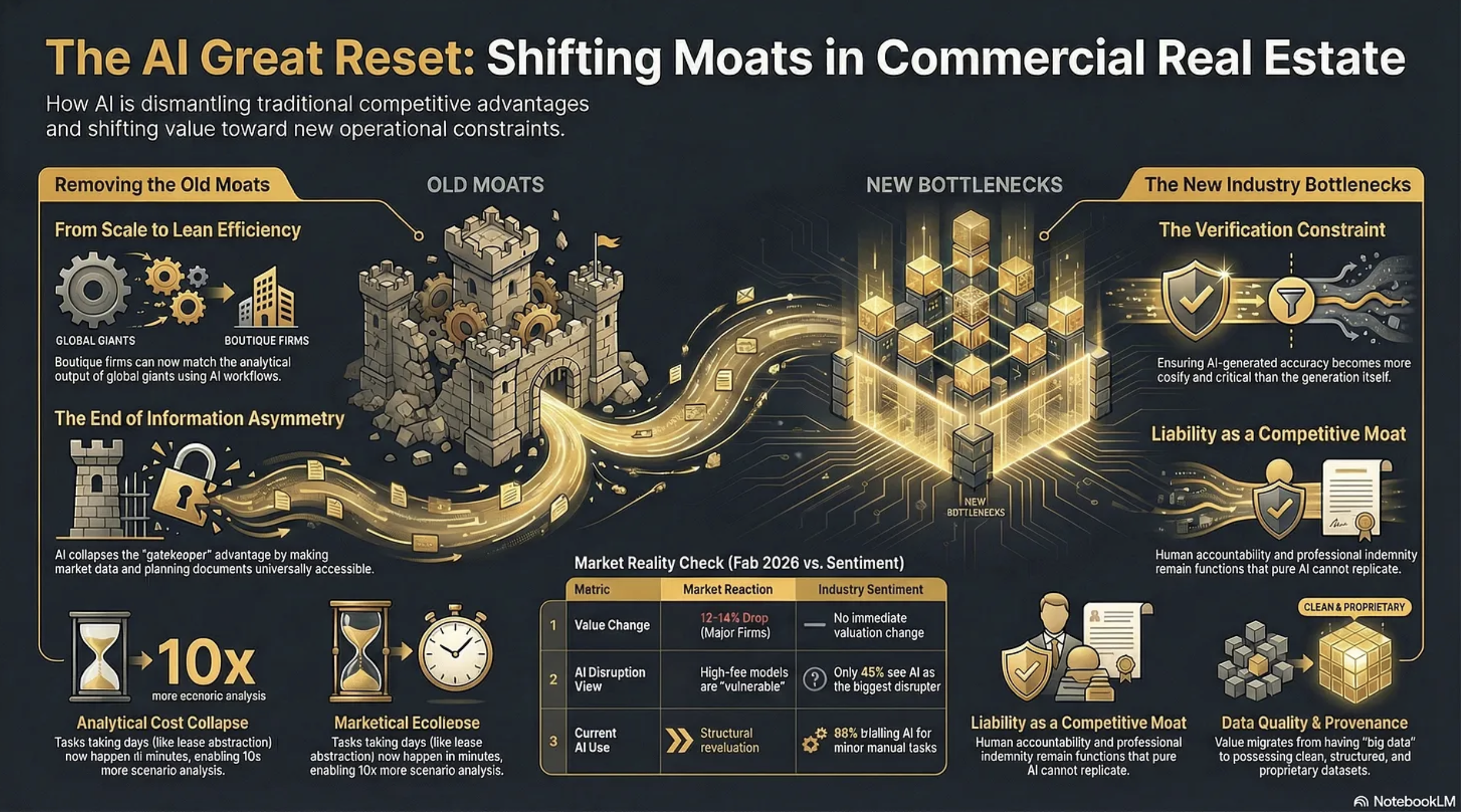

Two rather contradictory things happened on Wednesday, 11th February, 2026. First, shares in CBRE, JLL and Cushman & Wakefield fell precipitously on Wall Street, erasing circa 12-14% of their value. The consensus reason?

“We believe investors are rotating out of high-fee, labor-intensive business models viewed as potentially vulnerable to AI-driven disruption”

And then, on exactly the same day, PropTech giant Yardi put out a research report alongside the Association of Real Estate Funds (AREF) ‘examining how the real estate investment industry is responding to operational pressures through technology, data and digital transformation.’

Matt Glenny, commercial and investment management director at Yardi, describes the findings this way:

“The report gives us a real insight into the perception of the real estate industry compared to a lot of the hype that we hear. Just 45% of respondents see AI as the biggest tech disruptor of the next three to five years”

He adds that…

“88% of respondents are trialling AI in some form to automate or enhance performance of manual tasks such as reading and summarising documents and automating meeting minutes. Predictive analytics and the adoption of AI agents are viewed as future aspirations rather than a current consideration.”

So, the market and the industry are pointing in opposite directions.

Who is right?

Sangeet Paul Choudary, senior fellow at the University of California, Berkeley has written:

“New tech collapses old constraints. Once a constraint disappears, the logic of competitive advantage and business model design must be reimagined from first principles.”

If this is so then we need to look at what constraints AI is removing, what new ones it will impose, and how defensible are the moats underpinning current profitability within the CRE professional services industry.

What follows demonstrates the ‘Release’ phase of our RIRA Framework. Starting with…

CONSTRAINTS AI REMOVES IN CRE

Analytical Cost

Tasks that previously required teams of analysts working for days - lease abstraction, comp analysis, market research, financial modelling, due diligence document review - can now be performed in minutes. This makes existing work cheaper and, perhaps more importantly, it makes previously uneconomic work viable. The “non-consumption” opportunity is real: firms can run 50 scenario analyses where they previously ran 3, or screen 200 properties where they previously screened 20.

Knowledge Access

Information asymmetry - knowing things that clients and competitors don’t - has historically been a core source of CRE value. AI though will collapse this by making market data, comparable transactions, planning documents, and regulatory frameworks accessible to anyone with a well-structured prompt. The gatekeeping function that sustained brokerage margins will erode when the information itself becomes abundant. Proprietary data will exist, and still have considerable value, but far more information will become accessible than many realise.

Coordination

This is perhaps the least appreciated constraint that is being removed by AI. CRE transactions involve coordinating across multiple parties - lawyers, surveyors, lenders, agents, asset managers - each operating within their own systems and timelines. AI can interpret across these disparate data sources without requiring standardisation or consensus, compressing transaction timelines and reducing the friction that historically justified intermediary fees.

Talent Scaling

This is a fundamental constraint that AI is dismantling. A boutique firm with three sharp principals and well-designed AI workflows can now produce analytical output that previously required the likes of CBRE’s headcount. The scale advantage that the big companies enjoyed, hundreds of researchers, analysts, and junior professionals feeding the advisory machine, becomes less decisive when AI handles the analytical infrastructure underneath the senior relationship.

Geographic Knowledge

Deep local market knowledge - planning regimes, tenant dynamics, micro-location factors - has been a genuine moat for regional specialists. AI agents with access to planning portals, EPC data, Land Registry records, and local comparable evidence can approximate (not yet replicate) much of this knowledge, reducing the premium that locality alone commands.

CONSTRAINTS AI INTRODUCES

Verification

This becomes the new bottleneck. The more convincing AI outputs become, the harder hallucinations are to spot, and the greater the temptation to skip verification. This is a genuinely new constraint - the cost of ensuring an AI-generated IC pack is accurate may exceed the cost of generating it. Firms that build robust evidence architecture gain a real advantage; firms that don’t take on hidden liability risk.

Liability and Accountability

These create a structural constraint. When a junior analyst produces a flawed valuation, there’s a clear chain of professional accountability. When an AI system produces one, the liability question is genuinely unresolved. Professional indemnity, regulatory compliance, and fiduciary duty all sit awkwardly with AI-generated outputs.

However, this means that liability can become a moat. In knowledge work with ambiguous outcomes, absorbing liability remains a function that pure AI tools cannot perform.

Data Quality and Provenance

These constraints intensify. AI systems are only as good as their inputs, and CRE data remains fragmented, inconsistent, and often proprietary. The firms that have clean, structured, proprietary datasets gain compounding advantage. Those relying on the same publicly available data as everyone else will find their AI outputs commoditised immediately.

Governance and Workflow Design

These become a constraint on deployment speed. It’s not enough to have capable AI - you need checkpoints, audit trails, escalation protocols, and quality assurance routines. Building this infrastructure requires architectural thinking that most CRE professionals haven’t had to do before. The firms that solve the governance problem will be able to deploy AI at scale; the rest remain stuck in pilot purgatory.

Cognitive Dependency

This risk emerges as a longer-term constraint (though I believe a major one in the making). As professionals offload analytical tasks to AI, the institutional knowledge that informed those tasks atrophies. Junior professionals who never learn to build a model from scratch may lack the judgement to evaluate whether an AI-generated model is sound. Designing workflows and systemic methodologies to counter cognitive dependency will become a major requirement in knowledge businesses. I address this at length in my ‘Cognitive Sovereignty - Use It or Lose It’ article:

WHY CONSTRAINT MAPPING MUST BE WORKFLOW-SPECIFIC

These are generic constraints that are being removed or introduced across the CRE industry. They’re structural features of what AI does to knowledge work.

But the weighting differs enormously, and analysing them in relation to particular workflows is vital.

Consider the contrast between investment capital markets and property management. In capital markets, the information asymmetry constraint has historically been central to value creation, knowing about off-market deals, having proprietary comp data, and understanding institutional investor appetite. AI’s collapse of that constraint is existential to the business model.

In property management, information asymmetry was never the primary value driver: the constraints that matter are physical presence, emergency response capability, tenant relationship management, and regulatory compliance around health and safety. AI removes some PM constraints (reactive maintenance scheduling, compliance tracking, tenant communication at scale) but leaves the physical and relational constraints largely untouched.

Or compare valuation with development advisory. Standardised valuations face near-total constraint removal, AI can assemble comparables, model cash flows, and produce RICS-formatted reports with diminishing human input. Against that, on the new constraint side, there will be a need for professional sign-off and PI liability.

Other areas of the industry will be largely untouched by AI. Development advisory, for example, faces an irreducible constraint in planning committee politics, local authority relationships, and community engagement. The constraint AI does remove for development (planning application analysis, precedent search, viability modelling) is important but secondary to the human-political constraint that gates every project.

Then there’s leasing, where we’re seeing constraint-swaps. In the US, in multi-family, pricing has had constraints removed but that in turn has created a new legal constraint and we’re seeing several companies being sued over the ‘coordination’ of algorithmic pricing. That constraint doesn’t appear in capital markets or valuation work at all. It’s a constraint born from the interaction of AI capability with a specific regulatory environment (which arguably should have been anticipated).

So the constraint map - which constraints dominate, which are secondary, and critically, how they interact - has to be workflow-specific. And the interactions are where the real insight lives. Which is why our RIRA Framework has ‘Release’ as the first ‘R’ - you need to understand the new constraints that are appropriate to your specific workflow, or sector.

What is absolutely clear though is that AI is fundamentally changing the environment in which our businesses operate, and this in turn means that many of the moats we’ve relied on in the past might no longer exist.

THE FALSE MOATS

The Yardi/AREF report, together with Linkedin commentary on the stock price erasure, and pronouncements during earnings calls, make it clear that many in the industry believe CRE has special protection from several ‘moats’ that make it distinctive from other industries, and more defensible against AI.

These need to be addressed:

“Our relationships are our moat.”

Relationships are real, but their defensive value depends heavily on what those relationships enable.

If a client relationship primarily gives access to deal flow and information, AI erodes the information component. The relationship remains valuable, but the fee it commandscompresses because the analytical work underneath it requires less human capital.

The relationship is a moat for the individual, not necessarily for the firm’s margin structure. And crucially: relationships don’t scale, which means they can’t offset margin compression across the broader business.

“Our data is our moat.”

This is half-true, which makes it dangerous. The major companies do have proprietary transaction data, but much of it sits in unstructured formats, inconsistent taxonomies, and siloed systems. Having data and being able to use data as a strategic asset are very different capabilities.

Meanwhile, AI dramatically lowers the cost of assembling comparable datasets from public sources - Land Registry, planning portals, EPC databases, Companies House. The proprietary data advantage is real but narrower than assumed, and it’s a wasting asset if competitors build structured alternatives faster.

“Complex deals require human judgement.”

The definition of “complex” has been a moving target for decades (spreadsheets killed some complexity, databases killed more). What counted as requiring senior judgement five years ago (multi-scenario cash flow analysis, market positioning reports, tenant covenant assessments) is already within AI’s capability.

The residual, true strategic judgement under genuine uncertainty, is real but represents a much smaller slice of billable activity than the industry likes to admit. Is it more than 15%? Most of what brokers call “judgement” involves pattern recognition applied to structured data, which is exactly the capability profile where AI is advancing fastest.

“Regulatory complexity protects us.”

CRE is indeed heavily regulated; RICS standards, planning law, lease code compliance, environmental regulations. But regulation protects the activity, not the incumbent. AI systems that can navigate regulatory requirements more reliably than human professionals don’t erode the regulatory constraint - they erode the premium charged for managing it. Regulation becomes a moat only if firms combine it with liability absorption and governance credibility.

“Our brand and institutional trust are our moat.”

For trophy transactions - the £500m office acquisition, the major corporate relocation - institutional brand matters. Clients want CBRE or JLL on the cover page for their board. But this protects the top 5-10% of transactions by value. For the long tail of mid-market deals, where the analytical quality matters more than the logo, brand becomes less decisive as AI enables smaller firms to produce institutional-grade output.

“Scale is our moat.”

This is the one Wall Street is actively repricing. Scale was a moat when it provided analytical capability that couldn’t be replicated without hundreds of researchers. AI inverts this as it makes scale available to the lean.

It’s not hard to envisage a five-person firm with well-architected AI workflows producing the analytical throughput that required a 40-person team three years ago.

When technology collapses the constraint that justified your architecture, the architecture itself becomes a liability. The big companies’ headcount, which was their competitive advantage, becomes their cost structure problem.

THE MEANING FOR VALUE CREATION

So if AI is removing constraints, and creating new ones, and the industry’s moats are leaking fast, what does this mean for value creation?

The CRE industry is mistaking a stable playing field for a permanent one. Furthermore, it is thinking about how AI will support its existing operating models, rather than thinking about how to fundamentally change the game.

Last week the CEO of one of the major players said on an earnings call:

“that AI would benefit the business over the longer term, adding that its transaction and investment work would be “most protected” from disruption.”

Which encapsulates this thinking precisely.

The share price crash is the market, brutally and without nuance, beginning to price a structural revaluation into this sector. What the industry now needs to do is double down on understanding where value is migrating to. As analytical and transactional work commoditises, value will migrate to whoever resolves the new constraints - verification, liability, governance, and coordination.

Exactly what this means in terms of products and services is still to be determined. But by diving deep into the first ‘R’ in the RIRA framework, the map starts to become more like the territory, allowing us to better agree with or dismiss most of the ‘noise’ around CRE and AI today.

What is clear is that we have to think harder about where AI is taking us, and explain this precisely to the markets. The competitive advantage will accrue to those who can demonstrate why AI is a feature, not a bug. How many will manage that?

OVER TO YOU

What to do about all of this? What’s the strategic question you should be asking that you’re currently not?